Emerging Markets Debt: Strength, Resilience, and Opportunity

Emerging Markets Debt (EMD) continues to offer a compelling investment opportunity. As the global economic landscape shifts and geopolitical risks escalate, EMD stands as a pillar of prospect, offering attractive yields, solid credit quality, and a compelling risk-reward profile. This segment remains well-positioned for growth in a shifting macroeconomic environment, providing investors both return potential and diversification benefits.

1. Economic fundamentals remain anchored for EM countries

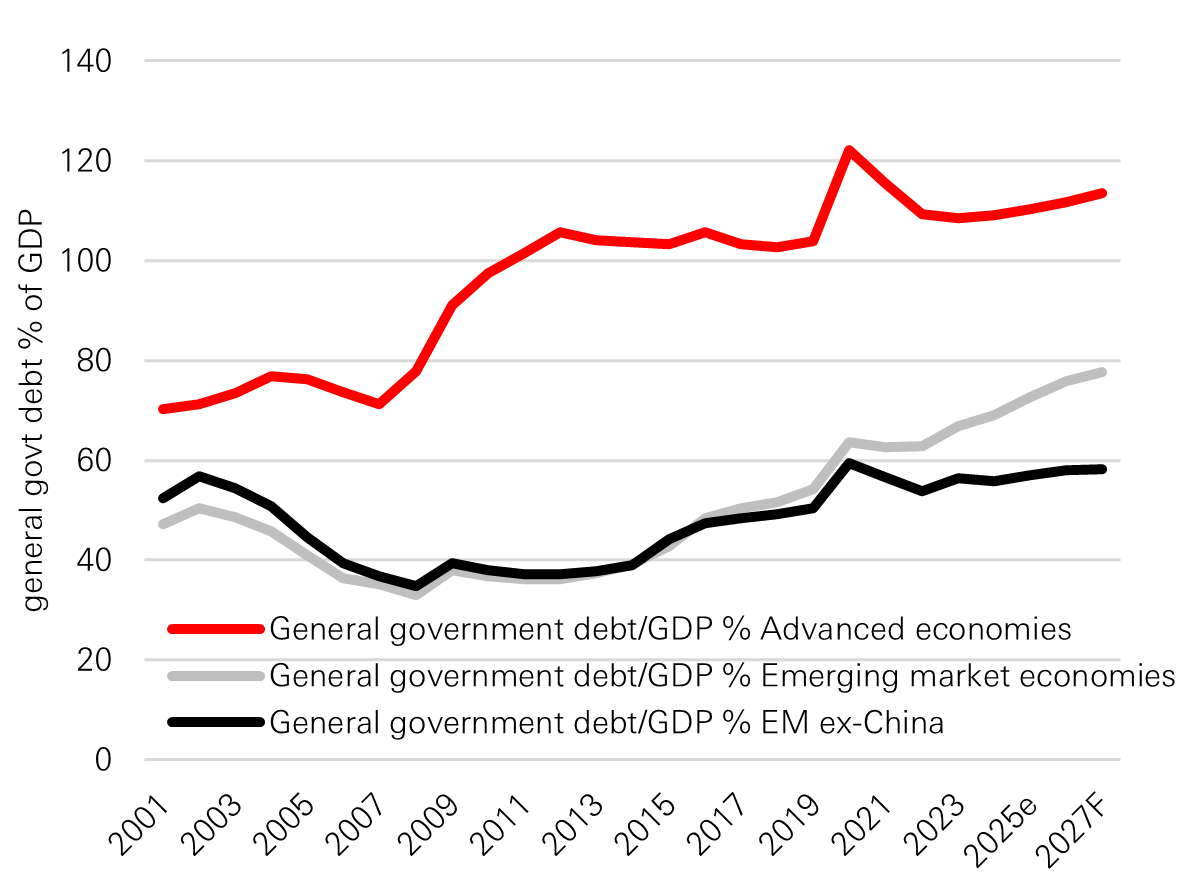

Central to EMD's appeal is the marked improvement in the fundamentals driven by fiscal discipline exhibited by many emerging market (EM) countries. Over the years, a commitment to sound fiscal management has bolstered their resilience, allowing these nations to weather geopolitical uncertainties, commodity spikes, tariff pressures, economic slowdowns, and external shocks more effectively than some developed markets (DM). Public debt to GDP ratio over the last 25 years in emerging markets ex-China have remained relatively stable, slightly below 60 per cent of GDP. During the same time period, the dual shocks of the global financial crisis and the pandemic have caused public debt ratios in advanced economies to rise over 30 percentage points of GDP.

Public debt has not grown at the same pace

Click image to enlarge

Source: IMF World Economic Outlook, and HSBC Asset Management, as of October 2025.

Source: HSBC Asset Management as of March 2026. This document provides a high-level overview of the recent economic environment. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. The views expressed above were held at the time of preparation and are subject to change without notice. This information shouldn't be considered as a recommendation to invest in the regions and currencies mentioned. Diversification does not ensure a profit or protect against loss.

2. EM Hard Currency Debt

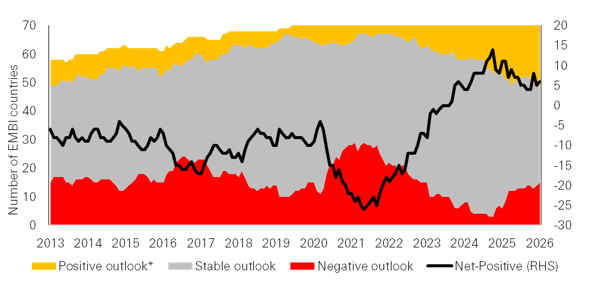

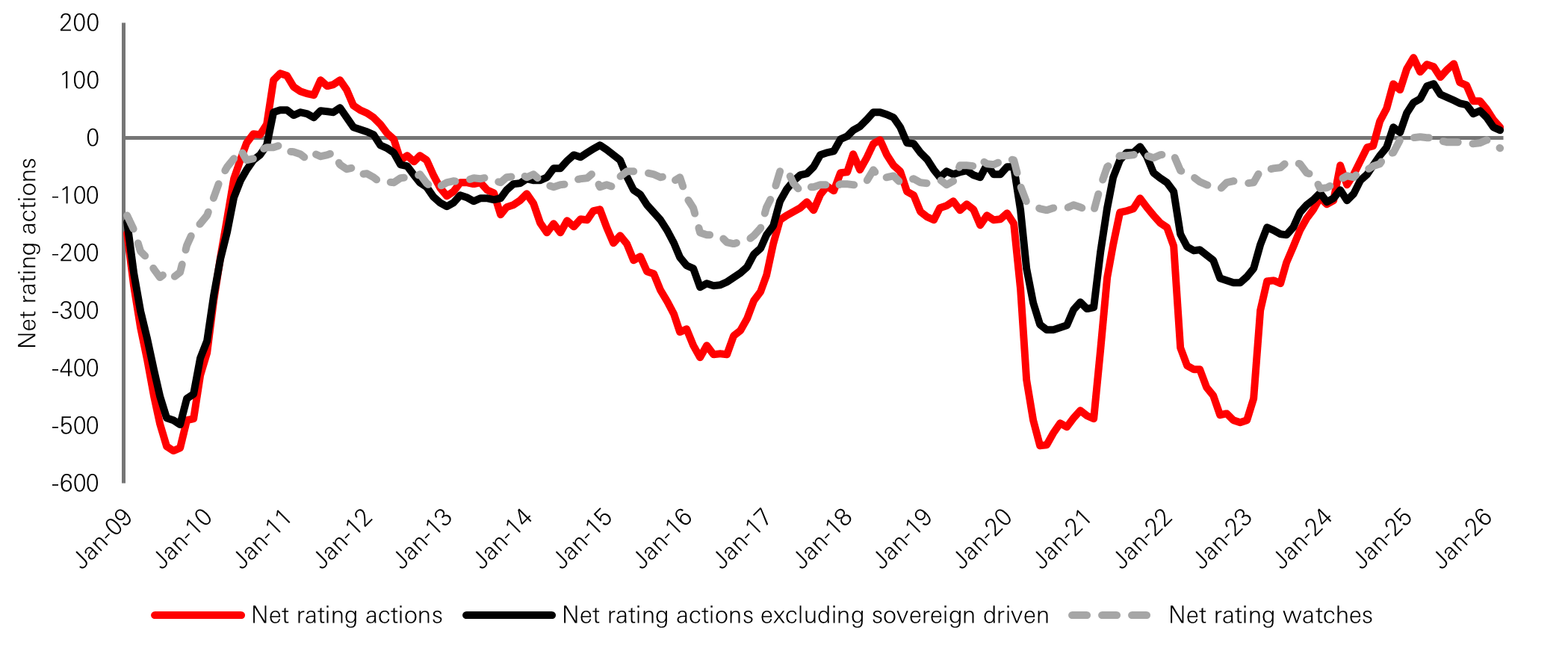

Credit rating agencies have increasingly recognized these improvements, with the average rating for EM sovereigns rising and issuers enjoying favorable outlooks and a high likelihood of rating upgrades in upcoming reviews. This trend, combined with improving fundamentals, underscores the growing strength of EM economies.

As a result of the improved fundamentals, EMs are better positioned to weather external shocks like the current spike in oil prices that has resulted from the conflict in the Middle East. EM credit spreads remain well behaved, reflecting the positive ratings story of EM countries, with upgrades across major economies like Argentina, India, Saudi Arabia and Turkey. Looking ahead, several smaller frontier countries are poised to gain investment grade status, including Costa Rica, Dominican Republic, Ivory Coast, Morocco, Paraguay and Serbia. EM corporates also benefit from the same constructive ratings context, with the 12-month rolling net credit ratings actions in EM corporates running at all-time highs and having turned net positive now in all EM regions. The carry of EM bonds remains attractive thanks to a higher-for-longer rates environment in the US, meaning asset allocators are not too late to join the EMD trade.

EM index countries' ratings outlook skew

Click image to enlarge

EM index countries' ratings over time

Click image to enlarge

Source: HSBC Asset Management, Moody's, S&P, Fitch, January 2026.

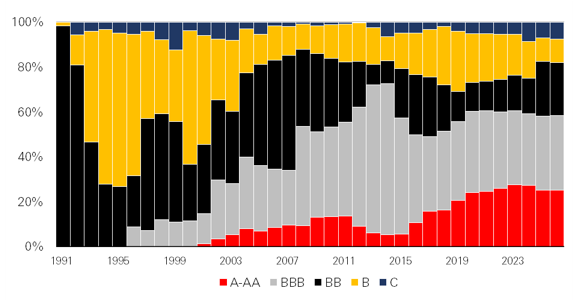

EM Corporate debt's value proposition is multifaceted, offering diversification, resilience, and attractive yields. Unlike U.S. corporates, which are heavily influenced by domestic economic cycles and Federal Reserve policy, EM corporates are not beholden to a single economic narrative. This diversification reduces the correlation risk, making them a stabilizing force in global portfolios. In addition, EM companies demonstrate stronger financial discipline compared to their DM peers, on average. They tend to have lower leverage, greater debt prudence, and more consistent currency risk hedging.

EM corporate credit - overall rating trends

Click image to enlarge

Source: J.P. Morgan, Moody’s, S&P, Fitch, Bloomberg Finance L.P., HSBC Asset Management, as of 31 March 2026. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way.

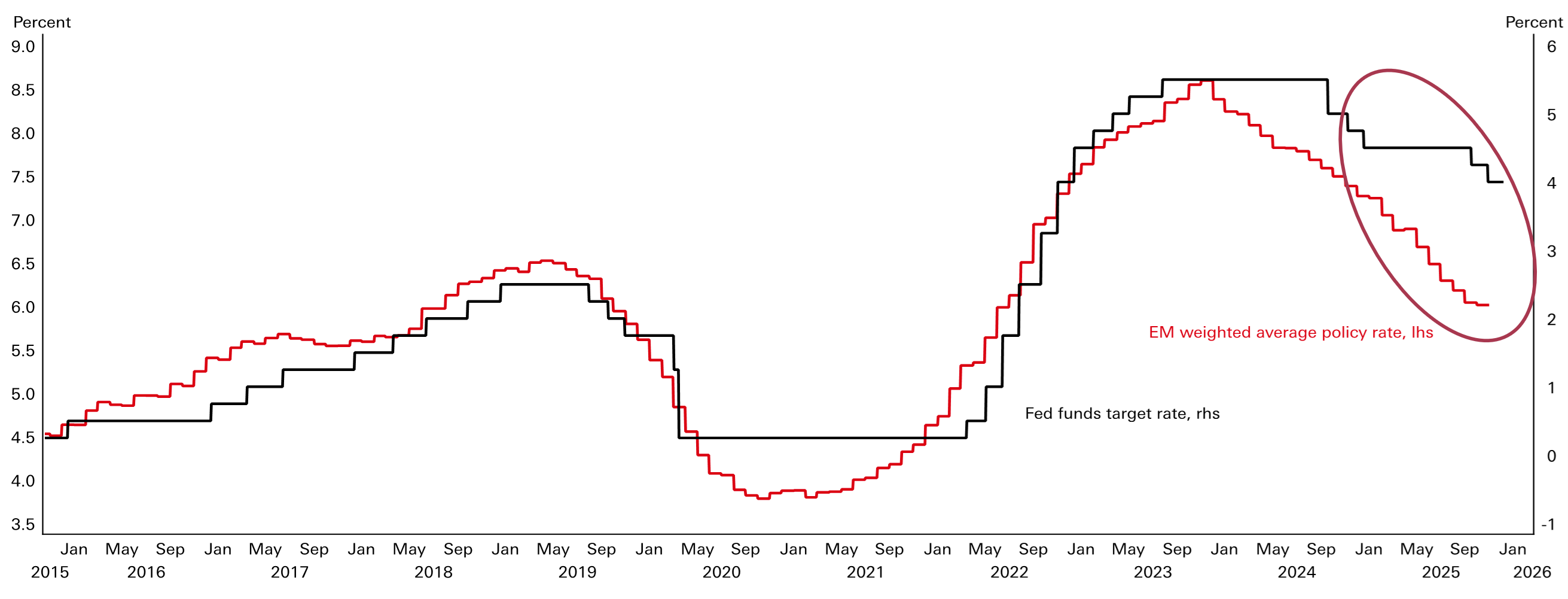

3. EM Local Debt

One of the things that stands out in this strong cycle for emerging markets is the fact that monetary policy has been so independent from the Federal Reserve. For the first time in history, EM central banks cut interest rates ahead of and faster than the Fed, owing to a more favorable inflation environment in EM relative to the US. The environment remains constructive given these factors, coupled with the likelihood that EM central banks to continue reduce interest rates regardless of the Federal Reserve policy stance. We expect that many EMs will continue to lower rates in 2026. This is not an isolated phenomenon but rather represents the maturation of the asset class and the growing strength and credibility of EM currencies and local bond markets. Additionally, a weaker US dollar, partly driven by questions around the safe haven status of US assets and US exceptionalism, could further boost EM currency returns.

Average EM policy rate vs the Fed funds target rate

Click image to enlarge

Source: Macrobond, HSBC Asset Management, January 2026. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

EMs to cut rates in 2026: Brazil, Chile, Egypt, Ghana, Hungary, India, Indonesia, Mexico, Poland, Romania, South Africa, Thailand, Turkey, and Uruguay

Source: Macrobond, HSBC Asset Management, January 2026. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way. The level of yield is not guaranteed and may rise or fall in the future.

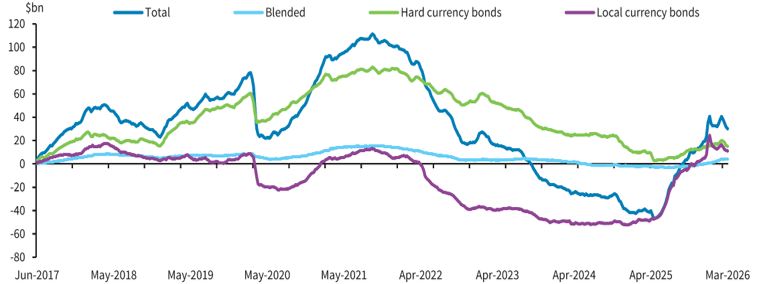

4. Under-Allocation Creates Room for Growth

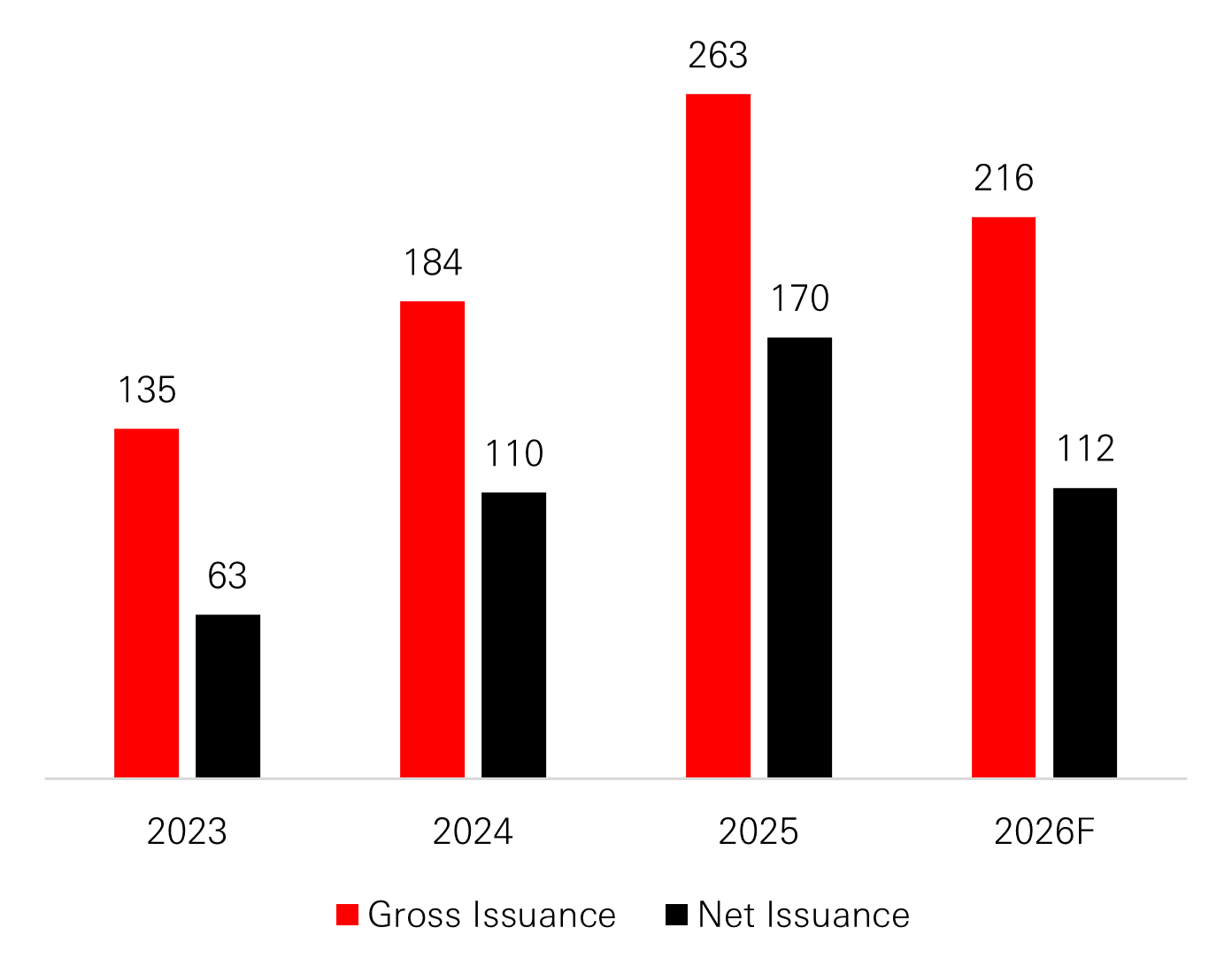

Despite these strengths, EMD remains under-represented in global portfolios driven by a legacy of cautious investor sentiment since the pandemic years. This under-allocation presents a significant opportunity for institutional and retail investors alike, as renewed focus on EMD is expected to drive substantial inflows into the asset class. The technical support from the increased inflows is occurring at a time of robust issuance across EM issuers.

EM Debt Flows

Click image to enlarge

Source: Barclays, EPFR, JP Morgan, February 2026.

Sovereign Issuance (USD billion)

Click image to enlarge

Conclusion

Emerging Markets Debt stands out as a strategic opportunity, combining resilient fundamentals, attractive relative valuations compared to DM, and ongoing improvements in credit quality. With the improvement in fundamentals, the EMD asset class has transformed. In the past, the universe was seen as dominated by lower rated, high volatility names – a segment to invest when chasing yields. Today, the asset class has matured with the majority of the top weighted countries in the index Investment-grade rated (JPM EMBIG Div). These are countries with strong balance sheets, credible policy frameworks, and real growth engines. Even within the high yield sector, many of these countries now have in place robust policy settings, solid external buffers, and improving credit metrics. Investors no longer need to sacrifice credit quality for yield, EMD offers investment-grade balance sheets with premium spreads.

With strong fundamentals, attractive yields, diversification benefits, and higher credit quality, EMD as a whole continues to be a strategic allocation for investors aiming to balance risk, reward, and opportunity in an ever-evolving global market.

Source: HSBC Asset Management as of March 2026.